Principles of Trust Funds: Accounting and Reporting

2.1 Responsibility

It is clear that the PCC should account in full for its incoming resources and for the way those resources are expended, but in many parishes it is not easy to identify just what the PCC is legally responsible for.

One of the principles of the charity accounting regime is that the charity trustees (here, the PCC members) should identify and include in their annual financial statements any resources that form part of their charity under ecclesiastical or trust law or that it controls and can benefit from.

The following are examples of situations that might arise. What are being described are organisations that may be connected with the church and whose funds may be under the control of the PCC to its own benefit in some way:

- The PCC may have parochial organisations (such as a men's group, a mother and toddlers group, or a church hall management committee) that operate as a part of the local church and are not controlled by another body (such as the Mothers' Union or the Girl Guides). The members may pay contributions that are used to cover the cost of meetings, refreshments, duplicating and speakers' expenses. The organisation may make a contribution to the PCC for the use of a meeting room or for the cost of heating and lighting.

- The PCC may also have funds belonging to it that are administered by members of the congregation, such as a flower fund to cover the cost of flowers in church or a choir fund with some of the money received for weddings.

- There may also be a 'friends' organisation or a parochial trust to which parishioners are invited to contribute.

- There may also be various other trusts, perhaps with the vicar and churchwardens as trustees, and with the passage of time the control of the funds may have appeared to move to the PCC or the purpose of the funds may have become uncertain (these may commonly be called 'vicar and wardens' trusts). The financial statements should include all the money and other assets entrusted to the PCC for whatever purpose, and show how they have been expended during the year and how the unexpended balance of each fund was held at the year end.

In all of these cases it is necessary to determine whether the income and costs belong to the PCC or to a separate charity or to a separate non-accountable body (e.g. a club or perhaps a 'corporation sole').

2.2 Is the PCC responsible? Questions to ask

Question 1

- Is this group so constituted that it is in law a 'special trust' of the PCC? (A special trust in section 287 of the Charities Act 2011 is defined as 'assets which are held and administered by or on behalf of a charity for any special purposes of the charity, and is so held and administered on separate trusts relating only to that property'.)

- If not, go to the next question.

Question 2

Does the PCC control the group? Related questions that may help to tease out the relationship concern whether the group has a separate constitution; whether it recognises the authority of the PCC; whether the group is a separate charitable institution. Using the church's name and registration with HMRC for reclaiming tax brings it under the PCC's control but just using the church's name in the group's title does not.

Question 3

Is the group under the control of some of the members of the PCC and are they acting as a sub-committee of the PCC in their control? If the PCC members outnumber the others in the control of the group, then the group is under the control of the PCC. The incumbent acting as a member of the PCC under its delegation may fulfil this function. For example, if the incumbent can restructure the control of the group, it is then appropriate to ask whether the incumbent is acting (i) in his/her own right or (ii) on behalf of the PCC. (It should be noted that the incumbent may be three bodies in one, with different capacities: acting in his/her own right as a person; acting alone as a 'corporation sole'; acting in a representative capacity as chair of the PCC.)

If i), then it has been established that the group is not under the control of the full PCC.

- If other PCC members are involved in controlling the group, the same question should be asked: i.e. are they acting (i) in their own right or (ii) on behalf of the PCC as a delegated committee?

- If (ii), then you are back to the answer to Question 2.

- If (i), then the question must be asked whether both sides think it is a connected charity - it is going to be 'connected' only by having parallel, common or related objects and being administered either in common with the PCC or by common trustees.

2.3 Applying the tests in practice

The following are examples of conclusions drawn from applying the tests:

- Funds raised using the PCC's charitable status to reclaim tax must be included within the PCC's financial statements. This applies to activities, such as a mission gift day, when the money will eventually be given away outside the parish.

- Monies collected by parochial activities, such as women's or men's groups that are not associated with a parent organisation and are not under the control of the PCC, need not be included. However, each organisation should be encouraged to account for its income to its members. If the PCC underwrites such activities (i.e. pays the bills if the organisers cannot) then they are within PCC control if the organisers cannot show otherwise - e.g. that the PCC only guarantees their creditworthiness but does not make decisions for them or claim their assets as its own.

- Monies that are collected by parochial organisations that are associated with a third party parent organisation, such as the Mothers' Union, are not included. These sums will be dealt with as a part of the financial statements of that organisation and any contribution made to the PCC for the use of meeting rooms will be received and recorded by the PCC, probably as a donation or as income from the letting of facilities. Those organisations should be disclosed in the Annual Report, explaining their relationship as associated charities working with the PCC in some way.

- Monies, restricted either as to their use or to their purpose, that have historically been collected by and from members of the congregation: usually these resources have been handled totally separately from the PCC accounts and the interest of the PCC treasurer is considered to be an intrusion. However, they are and should be accounted for, as restricted income of the PCC.

- A 'friends' organisation that raises funds for the upkeep of the church buildings: if the organisation is a registered charity, it will normally (especially if the PCC is not registered) account separately and file its own returns to the Charity Commission, but it will need to be mentioned in the PCC's Annual Report as a connected charity. If it is treated as an excepted charity under the umbrella of the PCC, then it is a branch and its accounts should be included with the PCC's financial statements.

A 'friends' or other charitable organisation that is not under the PCC's 'umbrella' might not have its own charity registration number. If it has exclusively charitable purposes and a gross income below the registration threshold (currently £5,000 a year), it is not required to register with the Commission but (if only to prove its charitable status) it should still have a written constitution and, like any other charity, must prepare annual accounts and behave charitably. If its income is above the registration threshold, then those managing it are in breach of charity law and should correct this by either registering as an autonomous charity or coming under the control of the PCC.

The PCC should not include in its own (entity*) financial statements the income or expenditure of a separately accountable, independent registered charity associated with the church (possibly the friends) - but the Charities SORP requires any material transactions between a related party and the PCC or any of its connected charities to be disclosed in the accounts notes. However, if the friends settle any PCC bills directly, that amounts to either 'donated services/facilities' or a grant to the PCC, which if Accruals accounts are prepared will then need to be accounted for as an incoming resource and as an appropriate expenditure. (*This means as distinct from group consolidated accounts, which are mandatory under the Charities Act 2011 only for groups exceeding £1m gross income - see Chapter 10.)

The specific accounting policies for any significant categories of income should be explained on the Accruals basis of accounting.

2.4 What are trusts?

A trust is a device in English common law to enable an appointed person or group of people to manage property (i.e. money and/or other assets) for a purpose specified by the trust's founder. The trust deed sets out how the trustees (of which there must normally be at least two, if individuals) shall manage or dispense the assets of the trust. Not all trusts are charitable. To be charitable the trust must have a purpose that is exclusively charitable in law and is for the public benefit.

There may be a variety of charitable trusts within the parish. In order to account correctly for these it will be necessary to identify and classify them. This may require some work depending on how carefully they have been administered in the past (although it should only need to be done once). However, accounting requirements apart, it is important to ensure that property held on trust is administered by the right trustees and used for the right purpose.

There may be some trusts that are not part of or connected with the PCC an will be subject to the normal registration and accounting regimes as with any other charity. These could include:

- The trust of a church school site and associated endowments held by trustees other than the PCC (e.g. the vicar and churchwardens).

- Other educational trusts not held by the PCC. Some parishes have Sunday school or religious education funds created by orders under section 554 of the Education Act 1996. These 'threefourteenths' trusts arise from the proceeds of sale of former church school sites. It was traditional for the incumbent to have use of the school for half Saturday and all Sunday - hence three-fourteenths - and the church school used the premises for the rest of the time. When the school is closed, threefourteenths can remain in the parish, normally under the trusteeship of the vicar and churchwardens (which was the traditional pattern for church school trusteeship). The trust, if it has an income over £5,000, will normally have to be registered in its own right and publicly accounted for by its trustees under the normal charity accounting rules. It is not 'a hidden pot of gold' which can be appropriated for the PCC's general purposes.

- Other vicar and churchwardens' trusts will also be separate charities unless they are special trusts of the PCC (see paragraph 2.5).

- Then there will be charitable trusts that are or may be connected with the PCC. They may simply have to be accounted for as one of the three main types of PCC fund, but it may be that they need to be 'tidied up' first to clarify what they are for, or that something can be done to make their administration more straightforward. Trusts in this category may be special trusts or they may be controlled charities of the PCC. The former are trusts of property held and administered by or on behalf of the PCC on separate trusts for any special purposes of the PCC:

- The property must be held on separate trusts (as could arise with a gift or legacy);

- It must be held and administered by or on behalf of the PCC, and so the trustees may not necessarily be the PCC itself;

- it must be held for a special purpose of the PCC and so a mere coincidence of objects is not sufficient - the trust must be for a part of the purpose of the PCC.

Therefore, a trust held by the vicar and churchwardens for general ecclesiastical purposes in the parish would not be a special trust of the PCC even though the PCC could also use its general funds for these purposes, but a trust held by the vicar and churchwardens for the express purpose of assisting the PCC in the maintenance of the churchyard would be a special trust of the PCC.

Sometimes, after carrying out all reasonable investigations, it will prove difficult or impossible to classify a particular trust or fund. If the amount involved is large it may be necessary to involve professional advisers to clarify the terms of the trust. However, if the amount is small so that the cost of unravelling the trust terms would be out of proportion to the value of its assets, parishes may wish to adopt a common sense approach and account for the trust as a special trust of the PCC or a controlled 'charity branch', so that at least it is accounted for somewhere.

2.5 Special Trusts

A special trust in section 287 of the Charities Act 2011 is defined as 'assets which are held and administered by or on behalf of a charity for any special purposes of the charity, and is so held and administered on separate trusts relating only to that property'.

2.6 Vicar and churchwardens' trusts

Trusts where the vicar and churchwardens are trustees generally fall into three categories:

Trusts for ecclesiastical purposes

E.g. maintenance of the church and churchyard: these are already required to be vested in the Diocesan Board of Finance (DBF) as custodian trustee. They will have similar objects to those of the PCC and will be included in the PCC's accounts.

Trusts for educational purposes

E.g. Sunday school funds arising from the sale of a church school: these are registered with the Department for Education. They are entirely separate from the PCC's financial statements; however, there may be cases where as 'connected charities' the existence of such charities is disclosable in the PCC's Annual Report, describing the relationship (e.g. the vicar is on both boards etc.) for the information of parishioners.

Trusts for the relief of poverty

E.g. to provide food or clothing for poor people in the parish: unless they are very small these should already be registered with the Charity Commission. Again, they are entirely separate from the PCC's financial statements; however, there may be cases where as 'connected charities' the existence of such charities is disclosable in the PCC's Annual Report, describing the relationship (e.g. the vicar is on both boards etc.) for the information of parishioners.

These trusts will normally need to be shown as a part of the PCC's financial statements. In exceptional circumstances they will need to be disclosed as 'connected charities' in the PCC's Annual Report and the relationship explained - in terms of any trustees and purposes in common and how the trust's activities dovetail with those of the PCC.

It should be noted that where incumbents and churchwardens, as the charity trustees of these trusts, have a legal responsibility to account publicly for them, any member of the public can ask for a copy of the statutory financial statements of such trusts.

2.7 What are funds and fund types?

Funds are the way in which Charity law requires you to track money given by your donors or received from other sources. Why is the government interested in this? They want people to be confident that the money they give for good causes is not misused or wasted but properly used. And, it is hoped, people will then continue to give!

People give to the church for all sorts of reasons. To help track the proper use of restricted money it is allocated to a fund of that type.

Most of the money a PCC receives will be for spending on the PCC's normal activities. This money is 'unrestricted income'. Sometimes the giver will specify particular activities that they wish the money to be used for. This money is 'restricted income'. Occasionally money may be given for the PCC to retain rather than spend on activities. This money is 'endowment capital'.

If you have unrestricted funds that the PCC want to use for a particular purpose, the chosen amount can be earmarked as an unrestricted 'designated fund' for that particular purpose. Each time you receive or spend money you need to say which fund it is for.

The following are examples of the names of some of these funds:

General fund

Bell fund

Church restoration fund

Choir and organ fund

Church hall fund

Legacies fund

General bequest fund

Sunday school fund

Building fund

Mission and charities fund

Fabric fund

Churchyard fund

Flower fund

Maintenance reserve fund

In addition, there may be funds in the name of the person who gave or left the money, possibly for a particular purpose.

Each of these funds is associated with a particular purpose or, in the case of some legacies, with the source of the funds. But the fund names do not immediately tell the reader of the financial statements whether they are held by the PCC on trust for a restricted purpose.

The word 'fund' has an additional use in charity accounting. As well as referring to money allocated by the PCC itself out of its general-purpose funds to be set aside for a particular use (e.g. fixed assets needed for the PCC to function) or project (e.g. to fund the provision of childcare or visits to special-needs parishioners), it is also used where the money is restricted in some way by the donor or by the terms of an appeal. With this latter meaning, each such fund is restricted by trust law, being either income that must be spent only on a specified purpose or else being capital (endowment) in nature that must be retained for the PCC's own use or for investment. In the latter case the investment income may or may not be restricted to spending on a specified purpose. It is important to know the difference between these types of fund as PCCs have to observe clear distinctions between them.

As stated above, many PCCs will already distinguish between all their funds by reference to the purpose to which they have been earmarked (such as those in the list above) or are restricted by law. For some, a clarification will be needed to record properly whether the fund is restricted (and if so, whether it is endowed) and for what purpose, or else unrestricted (and, if so, to confirm its status if designated for a particular purpose) in order to be able to demonstrate that the PCC has properly exercised the trust placed in it.

The charity accounting framework requires fund-based financial statements that in any case enable the reader to see that the PCC is spending its funds on the purposes for which they have been given. It may be helpful for smaller PCCs to give the project-based information, which is not required by law below the statutory audit threshold, as well as the funding aspect - i.e. surplus or deficit, either in a note to the financial statements or in the Annual Report (e.g. 'sales of the parish magazine exceeded printing costs by £140'). Even if not given in the financial statements, such information is likely to be important for the PCC in carrying out its responsibilities, and thus it may be appropriate to report such information in the 'Performance and Achievements' section of the Annual Report.

Hints and tips

Where possible use restricted money first. For example, if you have a youth restricted fund and the bill you are paying is for a youth event, it is likely that you can use this fund.

Why is this important? Restricted money can only be used for the purpose for which it was first given. Using restricted money when you can will leave more money in your general fund. This will give you the greatest flexibility to meet whatever happens later in the year!

When having a gift day or appeal, if possible make it for the general work of the church - this will give you the most flexibility when using the money.

If you have a specific appeal or gift day, make it clear that any extra money will be put into the general fund. For example, if you have an appeal for the roof which is so successful that the roof is repaired with £500 left over unless you have told people that any extra money will go to the general fund, this £500 must remain in the roof restricted fund.

Telling people what you will do if you get too much money (or if so little money that the project has to be aborted) means that they are fully aware of how their money will be used and so have the choice. It will also avoid having restricted money, that you cannot use.

When you claim Gift Aid on donations it must go to the fund to which the original money was given. This means that if a person gives you money for the youth work in the church it is restricted to youth work, and so is any Gift Aid you claim on that money.

2.8 Unrestricted funds

All PCCs have a general-purpose income fund, normally called a general fund, which they use to pay all the everyday expenses. This fund is 'unrestricted' because the money has been given to the church on the general understanding that it will be used at the discretion of the PCC for furthering the mission and ministry of the church. Unless specified otherwise, all the money received by the church is put into the general fund. Income generated from assets held in an unrestricted fund will be unrestricted income.

The PCC may decide to put some of the unrestricted fund money aside in other funds for use in the future (for example, for future building repairs). This money is 'designated' for these particular projects for administration purposes only. Designated funds are still unrestricted and can be moved to other general funds (redesignated or undesignated) if the PCC so decides. It is also important to bear in mind that these designated funds cannot at any time exceed the total amount of the general fund - i.e. you cannot earmark money for future spending before you get it, so they cannot leave you with a negative figure for the general fund's 'free reserves' (i.e. undesignated monies) but must be capped if necessary to avoid that. This is important because of the requirement to disclose in the Annual Report the trustees' policy on reserves, the actual reserves level at the year end and what is being done to bridge any gap between the aimed-for and actual levels of free reserves.

2.9 Restricted funds

PCCs also receive money that has been given for a particular purpose, for example:

- a collection in church may be announced as being for a particular purpose (such as the purchase of new hymn books or the repair of the tower);

- a fundraising event (such as a rummage sale or a coffee morning) may be held for a particular purpose;

- a donation may have been made or a legacy may have been left to the church for a particular purpose (such as the upkeep of the churchyard or the repair of the fabric).

All these sums have been restricted by the donor for a particular purpose and unless the donor has specifically reserved a right of consent to variation of purpose they cannot, and must not, be used by the PCC for any other purpose unless determined by the courts or the Charity Commission or else, for small trusts, the purpose is varied under the statutory powers given to trustees in the 2011 Act. Income generated from assets held in a restricted fund will generally be subject to the same restrictions as the fund the asset belongs to (unless the donor has specified otherwise).

An oral or written appeal or a collection for a special purpose, such as the fabric fund, will restrict the income to that purpose. There may be times when more money is raised than is needed for the particular purpose of the appeal. This excess money is restricted to the purpose and should be retained for use for the same purpose, or returned to the donors (except under the Gift Aid Scheme, which prohibits refunds).

This situation can be eased if the PCC acquires the power beforehand to use any surpluses for other purposes. The easiest way to avoid any problem is by announcing at the time of the appeal that any unused balance will be put to the general purposes of the PCC unless a donor explicitly forbids this (which would be a rarity). The restriction then applies until the purpose of the appeal has been satisfied. (A general notice to this effect can be placed prominently in the church to catch all occasions.) If someone wants to make a significant donation for a particular purpose, the donor could be invited to specify that they give the PCC permission to use it or a surplus for general or alternative specific purposes under certain conditions.

There could also be a potential problem if insufficient funds are raised for a particular purpose and the shortfall cannot be made good out of general funds. The PCC should always make clear in appeals what it would do if this situation were to lead to the project being abandoned - for example, to return all the donations (except where this is prohibited under the Gift Aid rules) or to use them for another related purpose.

When special collections (including any Gift Aid) are made to send straight off to other charities (e.g. Christian Aid, missionary societies) and the nature of the appeal is that there is no discretion for the PCC to do anything other than send the money directly to the charity, these are not funds of the PCC, as it is acting only as a collecting agent, and so the appeal should not be included in the PCC's gross income or total expenditure. It is good practice to include a list of these collections in the PCC's Annual Report, if only to confirm to the congregation that all appeals money collected has been duly passed on to the intended charity.

2.10 Endowment funds

Another form of restricted fund is known as an endowment. This is either capital money given to the church as permanent or (alternatively) expendable* capital with the specific instruction that only the income gained from investing the money can be spent, or it is a capital asset (such as a house) donated to be retained for continuing use by the church. (*If the donor has in any way authorised the spending of capital, it will be an 'expendable' endowment to the extent of the trustees' discretionary power to spend it.) The original money or assets (the 'capital') cannot be spent as income unless so authorised and must remain in the form of equivalent fixed assets (such as a house) or investments, but not necessarily the same asset that was given. It may be in a fund that is named after the donor.

There are thus two types of endowment capital, which must be distinguished in accruals accounts by note:

2.10.1 permanent:

a particular type of restricted fund where the capital, in accordance with the explicit requirements of the founding donor, must be held permanently. Any income return generated by the invested endowment (e.g. dividends) must be spent as originally determined by the donor, whereas any investment holding or disposal gain (less losses) belongs to capital on the same terms as the original gift.

2.10.2 expendable:

an endowment fund where the capital may, in certain circumstances, be spent. The PCC have this power, if given or implied by the donor. This fund is not income when it is first received, because there is no intermediate duty on the part of the PCC to spend it for its intended purposes. The PCC has the legal right (and even the duty) to retain the capital as capital and a further legal right to convert capital into income in accordance with the express or implied terms of trust imposed by the donor. However, if the power to convert is used, then at that time the amount converted becomes income. Any income return generated by the invested endowment will be required by law to be spent as determined by the donor without unreasonable delay and so cannot just be added to the retained capital unless a specific legal power to 'accumulate' income as capital allows this. Any investment holding or disposal gains (less losses) belong to capital on the same terms as the original gift.

Any expenses incurred in the administration of the capital fund (such as the fees of the person who manages the investments) should be charged against the capital of the fund unless the founding donor clearly intended otherwise. However, if the trust establishing a fund provides for it or if the capital fund has insufficient liquid assets to meet such costs (e.g. they cannot be used, as they consist only of land or buildings needed for the PCC's own use), the expenses can be charged to income (normally to the general fund).

2.11 Accounting for different types of fund

Where a PCC holds trust funds other than unrestricted funds, its accounting records must be adequate to allow separate accounts to be produced for each distinct trust fund. Restricted income funds and endowment capital funds must be shown separately in the annual financial statements. PCCs should also show in the accounts notes (if not in the balance sheet) how any designated funds have moved between year ends.

In the accounting records this administrative separation to comply with trust law can be done either by using separate columns in the cash book for the different types of trust fund or by clearly labelling each entry to distinguish those that are unrestricted and those that are restricted as to capital or as to income or merely designated.

In the annual financial statements unrestricted, restricted and endowment funds must be reported separately. As a minimum all funds of one type should be reported together, either as three separate columns (i.e. Receipts and Payments Accounts example) or, in the case of accounts on the Receipts and Payments basis, alternatively as separate statements of account. It is important that the reader can tell that the funds are not all held on the same legal basis and it is important that the PCC members know that certain funds have restrictions on the way the money can be used. The PCC must also be able to demonstrate that it still holds assets belonging to restricted and endowment funds and has not used these for unauthorised spending, nor for unauthorised purposes. It is a breach of trust to spend restricted income funds for purposes other than those for which they were given without the prior consent of the Charity Commission, or to spend trust capital without proper authority.

The PCC's unused monies, unless held for immediate spending, may need to be invested and investment returns generated. Any holding gains/losses and income earned belong to the fund whose assets were invested and so the income is subject to the same restrictions of purpose as apply to that fund. Therefore, the investment returns must be identified for each different fund, and in the case of investment pooling* this must be based on the amounts invested by each fund and the time for which they were invested, and then accounted for as part of the fund to which have belonged from the outset. (*Statutory authority for this is provided by the Trustee Act 2000.)

The only exceptions to this are:

- where the donor has expressly provided for some other use for the investment income;

- where the asset is part of a permanent endowment held for general purposes. In this case the capital is restricted in an endowment fund (because it cannot be spent) but the income is unrestricted since it can (and normally must) be spent for the PCC's general purposes or for any designated purpose.

If an endowment fund has assets (e.g. a house or investments) and any are sold, the proceeds of sale must be held within the same endowment fund. The same applies to the sale of investment securities belonging to a restricted income fund.

The SORP makes it clear that funds may be grouped and sub-analysed by major fund in the notes to the financial statements, and so all endowments may be reported on as one group, all other restricted funds as another group and all funds with no such restriction as a third group. It also requires the SOFA, balance sheet and any cash flow statement to show comparative figures for every item shown therein. PCCs have the option either to show the fund-accounting comparatives for all figures shown in the SOFA (using extra columns to do so) or else to show them in a 'prominent' accounts note.

In some cases other bodies of trustees may hold funds from which the PCC is legally entitled to benefit. If such trustees are only the custodians (i.e. they have no discretion over the use of the fund) then that money is a fund (in most cases an endowment fund) of the PCC. If the PCC does not have enough discretion over the use of funds held in its name to make it the 'charity trustee' of those funds, then they should not be accounted for in the PCC's financial statements. Instead, the fact of the fund's existence, its purpose and a description of the assets belonging to it should be disclosed in the PCC's Annual Report as custodian trusteeship holding, together with how the connected charity's activity relates to that of the PCC and how the necessary segregation of assets is maintained.

With parishes bearing an increasingly larger part of the costs of maintaining the Church of England it may seem odd to think that there may be parishes who have received income that they may find difficult to spend. Usually these will relate to restricted funds. Some examples might include the following:

- The PCC has investments in a restricted fund that are the proceeds of a house used for curates and parish staff in the past. This may be from a period in between employment of one staff member and another when a house has been bought in which it is possible that the parish is subsequently not required to house a worker; the PCC will then have to consider what to do with the fund.

- A building appeal fund has been set up but the proper permissions have not yet been granted and there is some doubt whether the project will go ahead.

- Money has been specifically raised to send an individual to undertake a specific project in a third-world country but because of a recent civil war that person cannot go or that project is stalled.

The status of such funds should be explained in the notes to the financial statements and any proposed action to dispose of the unexpended balances should be disclosed. This may include returning funds to the donors (subject to Gift Aid scheme rules) or obtaining permission (either from the donors (if, unusually, they had reserved to themselves a power of variation of the terms of trust) or by order of the Charity Commission) for the funds to be spent on other purposes.

Tips for handling different funds

- Clear records of restricted money should be kept so that it can readily be identified. Poor records can lead to confused administration and then it is possible that the rules will be ignored and restricted and unrestricted funds will be unlawfully merged with one another.

- Expenditure of restricted funds may anticipate promised funding at the time the expenditure is incurred. It is acceptable practice in such cases to show a deficit on the project and then wait for the promised funding before deciding what balance must be met from the general fund. However, any insufficiency of the general fund for this purpose cannot be made good out of other restricted funds. Where material, deficit balances on restricted funds should be shown separately on the face of the balance sheet, and not netted off against other restricted fund balances. Details of how the deficit is to be eliminated will also need to be given in the Annual Report (see Chapter 3).

- Collections at some funerals are taken in a bowl by the church door and are taken by the undertaker for a specific purpose at the wish of the bereaved family. These collections should only be recorded and accounted for by the PCC if the money is given directly to the church or the PCC makes the decision as to the use to which it should be put.

- Fees collected by the PCC (in the 'agency' capacity) for the services of bell ringers, organists, vergers or choir at weddings and similarly for organists, vergers and gravediggers at funerals (as with the collection of and fees belonging to the diocesan board of finance), should not be included in the financial statements if the money is paid over in full directly to those involved. In this case the PCC is acting as an intermediary and these fees do not count towards PCC income. PCCs will from time to time collect money on behalf of other charities in a public place or in church services. Examples of this include Christmas carolling and Christian Aid door-to-door collections. In these instances these receipts are not to be included in the PCC's income as the PCC is acting as an agent for the other charity. This is the case whether the money collected is sent off to the charity or if the money is counted and the PCC treasurer writes out a cheque for money paid into its bank account.

- PCCs should remember that they do not have to accept a gift if they are uncertain of its source or if they are not happy at abiding by the donor's conditions. All gifts for which the PCC reclaims tax under the Gift Aid scheme must be shown in the financial statements and its use agreed by the PCC. This would include the situation where tax is reclaimed on a donation paid under Gift Aid to be used for the PCC's charitable purposes at the minister's discretion.

- Legacies given for the general purposes of the PCC should immediately be credited to the general fund. Unless the donor has restricted the use of the legacy in the will, it remains unrestricted and may not be restricted by the PCC. All or a part of the legacy may then be designated for a particular purpose but it should not be designated to a 'legacy fund' with no intention as to its use.

- The separate administration of differently restricted funds does not require them necessarily to be kept in separate bank accounts, but this may be a useful practice in some circumstances as it does guarantee that they can always be identified as such.

- In the past, many parishes have operated with a large number of funds for different aspects of the church's life. Such a large number involves administrative complexity in the accounting system and the published financial statements. PCCs are recommended to keep under review the number of funds while taking care not to conflict with the strict rules on restricted and endowment funds.

- PCCs are advised to ensure that they have proper systems in place for the signing of cheques, the counting of collections (including the opening of planned giving envelopes) and their prompt payment into the bank.

2.12 Tips for handling other church funds

- The treasurer (on behalf of the PCC) should ensure that proper accounting records are kept by PCC 'branches' (organisations and those who hold the purses for small extra funds for which the PCC is accountable in law). Each year the treasurer will need to obtain an accurate return from each 'branch', which can be quite simple, consisting of a summary of Receipts and Payments for the year, and a list of any assets and liabilities at the year end. The figures from these organisations or funds should be added to the PCC's financial statements if they are material.

- Unless these 'branches' are a separately accountable legal entity, all the funds that they hold are the legal property of the PCC, whether or not they have a separate bank account.

- Friends' organisations not under the control of the PCC should be advised to have themselves properly constituted.

- Under the Ecclesiastical Fees (Amendment) Measure 2011, a portion of the parochial fees received is the legal property of the Diocesan Board of Finance with the remaining portion belonging to the PCC. These are separate fees: one forms part of the PCC's income while the other is the DBF's income (unless the fees are not assigned, when they will continue to be declared by the freehold incumbent whose stipend is reduced accordingly). It is therefore important that, when one cheque is received for both types of fee, the treasurer ensures that the relevant portion is paid to the DBF. Guidance to the Measure strongly suggests that in all cases (other than for non-assigned freeholders) incumbents should not handle fees, but that the PCC should be the local agent. The treasurer should not include the DBF's fee as part of PCC income in any way because they are only acting as an agent for the DBF when they collect fees on the DBF's behalf.

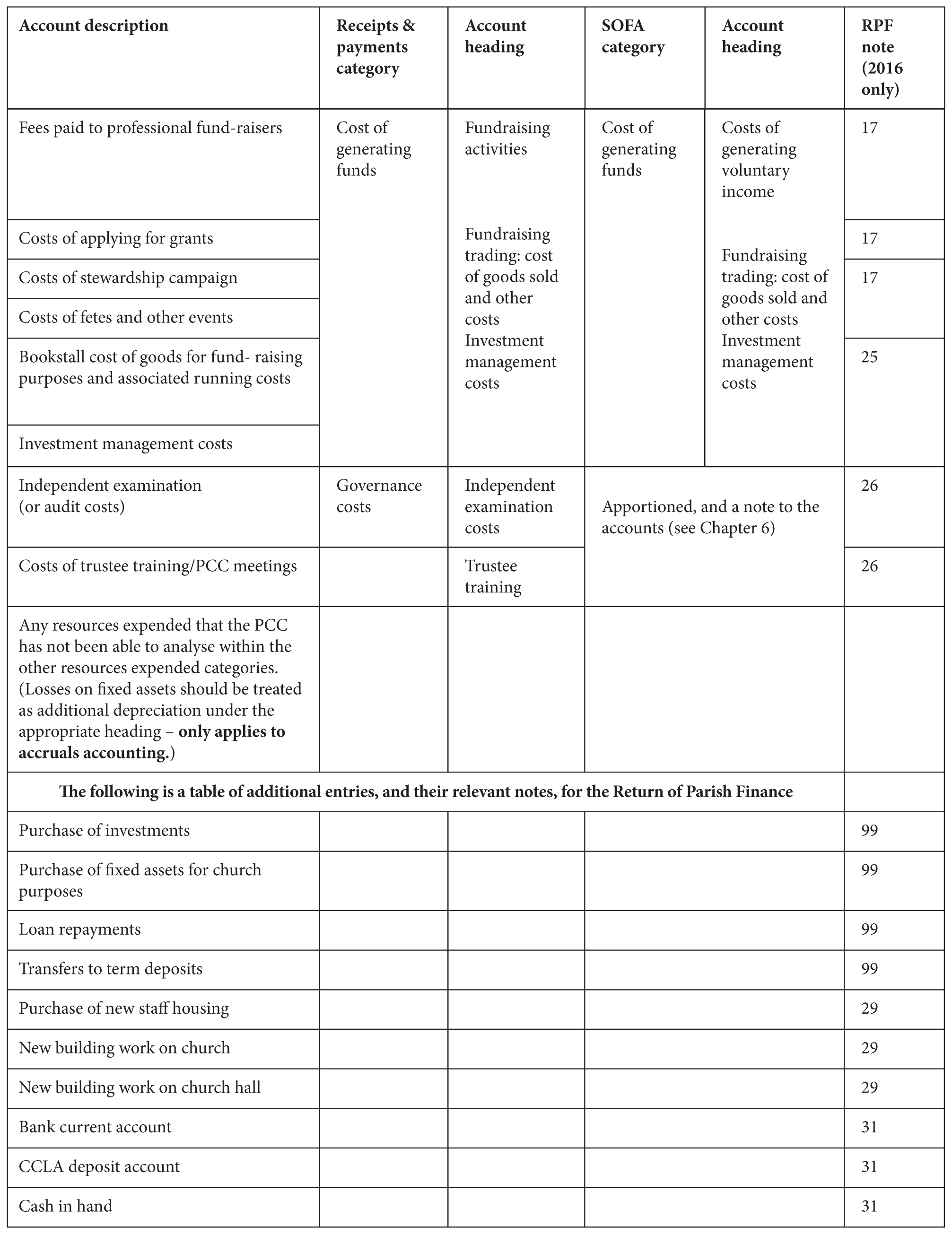

2.13 Categories of income and expenditure