Introduction and Legal Overview

1.1 Background

This publication has been designed to provide all users with a comprehensive and up-to-date reference guide to assist in the preparation of the requisite PCC Annual Report and accounts.

Introduction to Charity Accounting

Charities have a major impact on our society, funding or supporting community work that otherwise, if it would seem to be outside the total responsibility of government, would not happen! So it is easy to see why governments are interested in all charities. They want to ensure that money given to charities is spent on the charity's aims and not wasted, so that people will keep giving.

To achieve this aim successive UK governments have been developing charity law for more than 400 years. They have made charity trustees more and more responsible for the work and finances of the charity. The members of the PCC are charity trustees. The Charities Act (2011) defines charities as organisations that aim to provide 'public benefit' in one or more charitable areas or 'purposes'. It has also reinforced the Charity Commission's legal powers to be able to support and regulate charities.

The Charity Commission created the Charities SORP ('Accounting and Reporting by Charities: Statement of Recommended Practice'), to give us clear guidelines on what information to keep and what reports to produce to meet our legal obligations. The Church of England has adopted the SORP as its standard basis for annual financial reporting by parishes, so that now we can provide the same information to both the government (for the general public) and the wider Church.

What does this mean for you as a parish?

As PCC members we are the charity trustees of the parish. We therefore need to understand what money is coming into the church, how we are spending it and why. In order to give a clear account of how the money has been received and spent, each parish has to produce the reports required by law.

These accounts and reports help us to tell people how their money supports the mission of the church. They will also help us to show that the money given to us for running the parish or for specific aims such as youth or building work was used for those purposes. As PCC members we are responsible for the money, how it is looked after and for providing clear information about all of the money that belongs to the church.

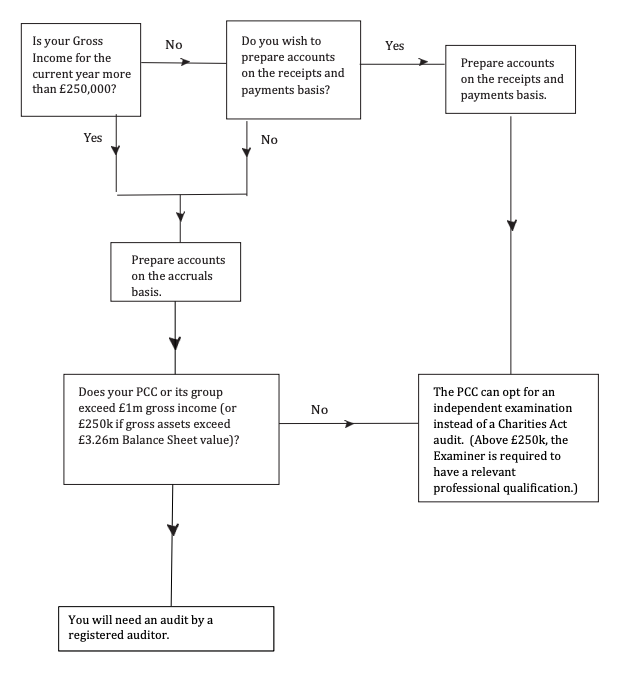

The first step in providing the correct reports is to decide which kind of annual accounts you need to produce and how these will be externally examined. There are two alternative ways of preparing annual accounts: either the Receipts and Payments basis or the Accruals basis.

The reader can select the relevant chapters depending on whether they are producing accounts on a Receipts and Payments basis or are adopting accruals accounting. The following flow chart is the starting point and should be used to determine which method should be adopted. Chapters 5 to 8 provide detailed guidance and examples for each method, while Chapter 9 includes guidance on moving from one accounting to another.

This revision of the guide has been produced by sub-groups of the Diocesan Accounts Group. The sub-groups comprise representation from diocesan and national church staff and external professional advisers. The members of the sub-groups are acknowledged at the back of this guide.

The content of this book is accessible online on the Church of England's Parish Resources website at: www.parishresources.org.uk.

Further guidance can be found on the Charity Commission website at: www.charity-commission.gov.uk. Another useful source of guidance is the Association of Church Accountants and Treasurers (ACAT). This is a national charity that provides resources to support the work of treasurers in churches of all Christian denominations. ACAT provides a programme of training events including foundation courses for new treasurers and more detailed workshops on specific topics that are relevant to PCC governance and financial administration. Further information is available on ACAT's website: www.acat.uk.com.

1.2 Regime of public accountability

There are two different bases for the preparation of annual financial statements, depending on the size of the PCC in terms of gross annual income. There are also two different forms of external scrutiny of the financial statements.

The requirements and options are summarised on the following flow chart.

1.3 Making the choice

This section describes whether accounts on the Receipts and Payments or Accruals accounting basis must or may be prepared.

In order to discover which aspects of the Regulations apply to the PCC, its statutory 'gross income' must first be calculated according to the Charity Commission's rules. The PCC can then identify where it stands in the accounting framework for charity accounts.

The Charity Commission's rules for calculating gross income allow you to do this by reference to cash receipts as long as the figure of £250,000 is not exceeded on that basis. If it is exceeded you will have to prepare accounts on the Accruals basis, even if this would result in showing a gross income figure of less than £250,000 in the Statement of Financial Activities (SOFA).

If the PCC's income for the year exceeds £500,000, the PCC is deemed to be a 'larger charity'. There are then extra disclosure requirements for the Annual Report and the accounts and a cash flow statement is mandatory under FRS 102.

How do you decide? The basic rule is to calculate the gross income of your parish (that is all monies received as income before any payments have been made out of them or any costs deducted, and excluding any trust capital monies received for endowment or any loan monies). If the total is:

• Up to £250,000 for the year, you can choose to prepare either Accruals accounts or the Receipts and Payments-based accounts.

• Over £250,000 a year, you must prepare Accruals accounts.

If your income is up to £250,000 per year, Receipts and Payments is the easier form of annual accounting for your parish. Unless there are particular reasons why accruals accounts are needed for your parish, new treasurers are advised to choose Receipts and Payments.

Accruals accounts are required by law if the PCC's annual gross income is over £250,000.

1.4 What is the gross income of the PCC for the purposes of Receipts and Payments accounting?

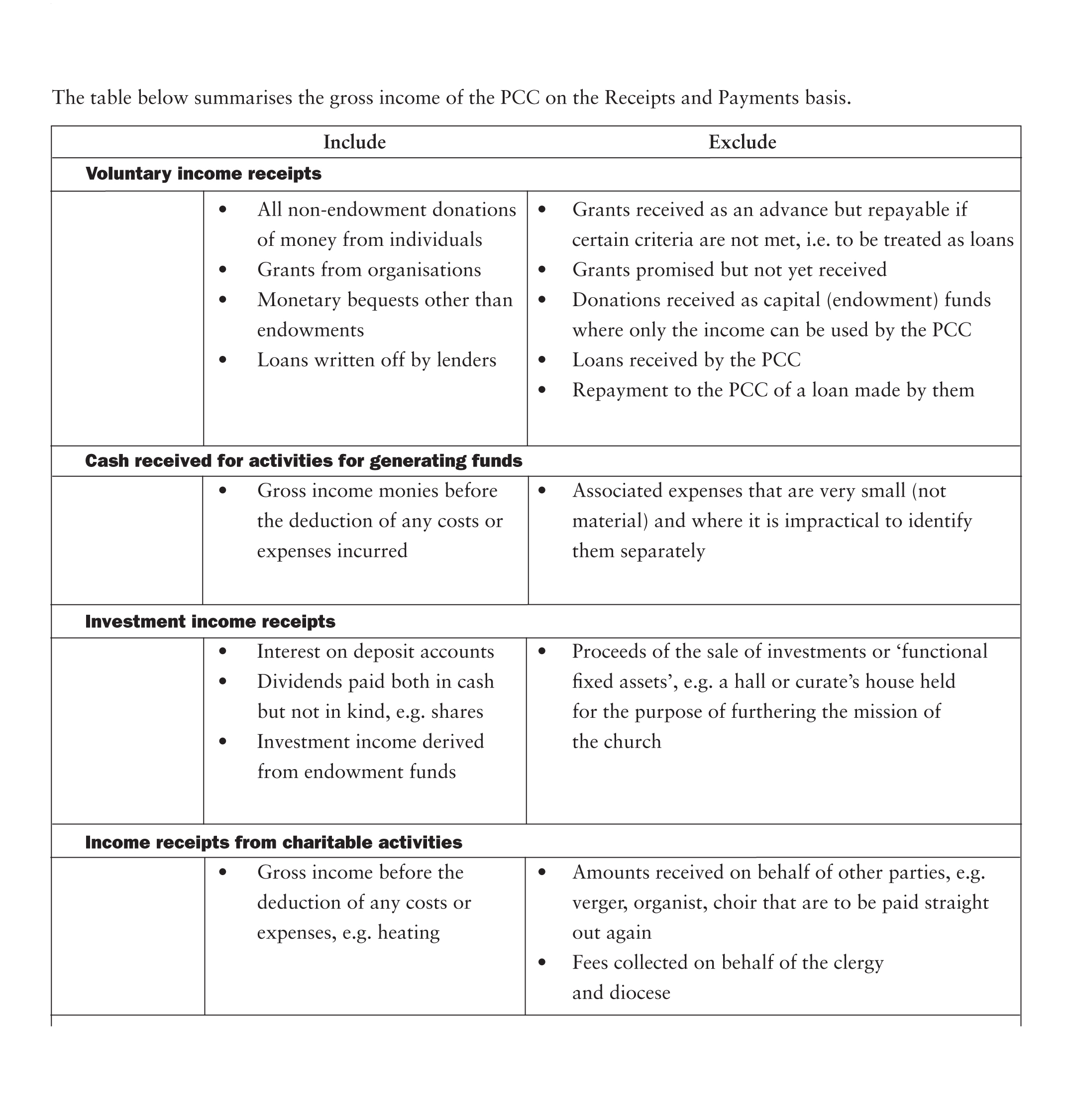

The gross income is the total amount of money recorded as income of the PCC in all unrestricted and restricted funds but not amounts of money received as capital (endowment funds), nor the proceeds of disposal of any assets held for investment use or for the PCC's own continuing use. Gross income receipts should be recorded before the deduction of any costs or expenses and includes the following:

• Money received as voluntary income;

• Money received from activities for generating funds (fundraising for church activities);

• Investment income receipts;

• Receipts from fees and charges for charitable activities;

• Any amounts of money taken out of endowment capital as income during the year (i.e. transferred into income funds or otherwise spent as income).

The following items should be excluded:

• a loan received by the PCC;

• the repayment to the PCC of a loan made by them;

• the proceeds of the sale of investments or 'functional fixed assets' (such as a hall, which is held for the purpose of furthering the mission of the church) or any gain or profit on their sale;

• donations grant or legacies received in money by the PCC as endowment capital.

Where a PCC holds endowment funds, the following items must be included in the gross income calculation:

• any permanent or expendable endowment spent, borrowed or spent as income and therefore transferred to income funds during the year;

• any permanent endowment 'unapplied total return' allocated or transferred to income funds during the year.

Further detail of the various items of income is given in Chapter 2.

Points to note

• In calculating the gross income, there should be no netting off of expenditure and income (no cancelling income against expenditure). Suppose the parish runs a fete and raises £1,000 after charging £500 for expenses. They should show £1,500 of income and £500 of expenditure. If the netting off is small and it is impracticable to identify the precise amount, then this requirement to 'gross' up can be ignored.

• If in doubt, include an item rather than leave it out - unless that takes the PCC into costlier regulatory regime (e.g. statutory audit) when professional advice will be needed. The rules are to help people to understand the financial statements more easily and to help PCCs have the information they need for managing their affairs properly. These aims should be kept in mind when deciding which small items should be included or excluded, either gross or net.

• Money may be received to build a new building or to improve an existing building. If the funds raised create an endowment (due to the capital nature of the project for which the donor intended the gift to be used, i.e. to equip the PCC with assets for longer-term use), or the asset to be improved is an endowment asset, the funds raised are endowment and should be excluded from the calculation of gross income.

• If there is a major appeal for activities or repair or a major non-endowed legacy is received in a year it will be quite possible for the gross income in that year to increase from, say, £100,000 to over £250,000. If this happens, no attempt must be made to manipulate the figures by artificially accelerating or delaying activities. As the PCC will be handling larger sums of money it is only right that it should have to account for them in a more rigorous way.

• The law requires all gross income to be included (e.g. any occasional non-endowed legacies and grants), even if its inclusion makes the financial size of the parish much bigger than was previously the case and than the PCC expects. The calculations are made to arrive at a figure of genuine gross income.

Legal overview

This section provides an overview of the requirements of the Charities Act 2011 and associated regulations and relates them to both large and small Parochial Church Councils.

1.5 The duties of the PCC

The members of the PCC are the charity trustees and are the 'persons having the general control and management of the administration of the charity' (Charities Act 2011, s177).

The trustees are entrusted with the PCC's funds. They must:

• Always act responsibly;

• Ensure that all decisions are taken for the benefit of the PCC;

• Always act in accordance with the governing documents, principally the PCC (Powers) Measure 1956 as amended by the Ecclesiastical Property Measure 2015;

• Not seek personal benefit (commitment to the cause must be the main reason for serving as a trustee).

The PCC is responsible for all parish finance, its management and control, including the appointment of a treasurer. While it may delegate some of its duties, for example, to District Church Councils (DCCs), this does not remove its legal responsibilities. These include:

• Keeping 'proper accounting records', which include the annual financial statements, and which must be preserved for at least six years from the end of the financial year to which they relate. The records must be sufficient to:

- show and explain all the PCC's transactions;

- disclose the PCC's financial position at any time with reasonable accuracy;

- enable the required statutory accounts to be prepared;

- show on a day-to-day basis all Receipts and Payments and what they were for;

- record all assets and liabilities.

• Ensuring that the finances of the PCC are under its control and decision making is only delegated if the PCC can ensure that its wishes will be followed.

• Arranging for a suitable independent examination or audit of the financial statements.

• Preparing the Annual Report and accounts (financial statements), which must be presented to the Annual Parochial Church Meeting in accordance with the requirements of the Church Representation Rules.

1.6 Accounting framework

The accounting, auditing and reporting regime for Church of England PCCs is contained in the following documentation:

• Charities Act 2011

• Charities (Accounts and Reports) Regulations 2008

• Statement of Recommended Practice on Accounting and Reporting by Charities SORP (FRS 102)

In addition, financial statements for PCCs must be prepared in accordance with the following:

• The PCCs (Powers) Measure 1956

• The Church Representation Rules (CRRs)

• The Church Accounting Regulations 2006, which form the link between the CRRs and the requirements of the Charities Act.

The law makes it clear that charities are accountable to the public for the resources they control. Charities receive funds for public benefit and must demonstrate to the public that they have observed the trust placed in them in the handling and use of those funds.

Under the Charities Act 2011, all PCCs below the special registration threshold (currently £100,000 per annum) are excepted charities and do not have to file annual returns or Annual Reports and accounts with the Charity Commission. Details of the registration process for PCCs over this threshold are available on the Parishes Resources website (www.parishresources.org).

All PCCs must prepare their Annual Report and financial statements in accordance with the Charities Act 2011 and the regulations and, as with any other charity, must make them available to the public.

1.7 Accounting for the legal entity

The general principle is that statutory accounts must be produced for the legal entity.

That means that PCCs (as the legal entity) must prepare appropriate Annual Reports and accounts that are in accordance with the Charities Act and the Charities (Accounts and Reports) Regulations, as applicable, and this responsibility cannot be delegated to others.

This is quite straightforward in most cases but questions arise when considering teams, united benefices and pluralities.

1.8 United benefices and pluralities

The legal entity is the PCC and not the united benefice, team or plurality, and it is the PCC that must produce accounts in the statutory format.

The thresholds are tested for each PCC, which must each appoint an independent examiner or, if appropriate, an auditor. Providing the independence test holds good, the same person may agree to serve more than one PCC.

1.9 Teams

Teams vary a great deal and the guidance on how to meet the requirements of the Charities Act varies with the circumstances. For example:

• Teams that comprise a number of separate PCCs must produce separate accounts that meet the statutory requirements at the level of each PCC. Of course, a summary financial statement can be produced at the level of the team, but there is no requirement to do so and there are no constraints on the format.

• Other teams may have been formed on the basis of a single parish comprising one PCC with more than one place of worship but without DCCs. As before, accounts that meet the statutory requirements must be produced for the PCC. Of course, there is nothing to stop the production of non-statutory financial statements that in each case relate to one of the different congregations with its place of worship, but there is no requirement to do so and there are no constraints on the format. It may be appropriate for such information to take the form of notes to the PCC accounts (so that they are part of that body of statutory information).

1.10 District Church Councils (DCCs)

A situation may arise where pastoral reorganisation has combined separate parishes into a new single parish and thus a single PCC with DCCs as its 'branches' to retain the sense of local community.

In both these cases statutory accounts must be produced at the level of the PCC, though these can of course be based on the aggregation of 'branch' accounts that may be produced by the DCCs for their own congregations.

While certain internal management responsibilities can be passed down from the PCC to its DCCs, this does not amount to delegated legal and financial responsibility, which must by law stay with the PCC as the only body with legal standing. DCCs cannot have assets of their own, they do not have body corporate status like the PCC, nor are they legally distinct from it, and so they should not be taking financial decisions and signing contracts, for which they lack the requisite legal standing. Of course, the PCC can decide to leave DCCs free to operate within an agreed budget, but the PCC is the only legal entity that is able to enter into a contract or institute legal proceedings.

Where DCCs have been preparing their own accounts there is no reason why this should not continue, but these are then only 'branch' accounts, to be brought together at the PCC level to form the latter's statutory accounts, and therefore careful co-ordination between the DCCs and the PCC over the final examination/audit of the PCC's statutory accounts will be needed.

1.11 Aggregation of PCC and DCC accounts

If the DCCs have been used to preparing and publishing their own, separate accounts, the need to aggregate the accounts at PCC level may be a cause for concern to them. Consideration of the following may mitigate the circumstances for them:

• If the DCCs are very small and the PCC of which they form a part is below the accruals accounts threshold, the statutory requirements should be relatively easily met by taking the Receipts and Payments accounts for the individual DCCs and preparing a combined statement of receipts and payments to go with the PCC's statement of all assets and liabilities. An Annual Report will be required at PCC level which could have general details for the PCC and short reports on activities from each DCC.

• If the aggregated gross income exceeds £250,000 per annum, then the statutory requirement is for a single statement of accounts on the accruals basis covering all the DCCs and other transactions at PCC level. It should be noted that if either the gross assets threshold of £3.26m is exceeded at this level of income or else (regardless of balance sheet considerations) the income threshold of £1m (£500,000, per annum prior to 2015) is exceeded, then the accounts must be audited. The group accounting threshold is also £1m.

• The independent examiner's task may appear onerous but the person responsible for the examination does not have to carry it all out themselves. The PCC will need to appoint an independent examiner (who will need to meet the requirements of the task) but the examiner might choose to delegate aspects of the work to others, particularly if a number of congregations have to be covered. In this way each DCC may have its part of the aggregated accounts examined by a different person, but the DCC examiners would all be working to the PCC's statutory examiner, who will take sole legal responsibility for any work they have been delegated to carry out. It is the PCC examiner who is responsible for agreeing the programme of work of the local examiners, reviewing the results of their work and then reporting in statutory terms on the statutory accounts of the PCC.

It cannot be avoided that aggregation at PCC level may increase the gross income of the PCC to a level that means that it crosses a threshold and enters a more rigorous regime.

It should be noted that a PCC with DCCs does not require a common bank account. The PCC may arrange for each DCC to have its own bank account but this will need to be subject to the overall control of the PCC and subject to an assessment of any risks and benefits of operating multiple bank accounts.

Joint arrangements

Some groups of PCCs operate a group or PCC account, to which PCCs contribute. It is used to fund joint activities, such as the incumbent's working expenses or a magazine. This fund may be accounted for in one of two ways:

• One PCC in the group may control the fund as a restricted fund and receive grants from the other PCCs in the group. This PCC then accounts for the fund and the other PCCs show their contribution as a grant. If the fund is a significant sum of money, the PCC may not wish to adopt this method as it may move them into a more complex accounting regime.

• The joint account may be handled as an informal 'joint venture' (called a 'joint arrangement' in the SORP), where each PCC accounts for its share of the total fund. A PCC treasurer may operate an account, which serves the joint activity. The expenditure on the account should be allocated appropriately to each PCC. The PCC treasurer running the account should not treat payments received from the other PCCs as income. Any assets or liabilities generated within the account also need to be allocated to each contributing PCC at the year end.

1.12 Local ecumenical partnerships (LEPs)

Where a parish is part of a Local Ecumenical Partnership (LEP), the Annual Report and accounts must be prepared in accordance with the constitution for the LEP. Some denominations have a year-end date other than 31 December and the constitution will establish the relevant accounting date for the particular LEP. The constitutions may establish different legal rights and obligations for the participating denominations and the accounting consequences will need to be determined on a case-by-case basis.

1.13 Registration with the Charity Commission or excepted status

The Charities Act 2011 specifies that PCCs and other excepted charities with gross income in excess of a special registration threshold (currently £100,000 per annum) must register with the Charity Commission.

Dispensation from registration can be sought from the Charity Commission where the income threshold of £100,000 per annum has been exceeded only because of an exceptional and non-recurring item.

Details of the registration process are available on the Parish Resources website (www.parishresources.org).

Registered charities must:

• disclose their registration status on all relevant documents, e.g. letterheads, website, cheques, invoices and receipts (e.g. a registered charity or Charity No. xxxxxxx);

• submit an annual return to the Charity Commission;

• submit a copy of the annual report and accounts to the Charity Commission (unless PCC income has fallen below £25,000 for the year).

Excepted status remains for all PCCs that are not registered with the Charity Commission.

Excepted charities do not have a charity registration number and do not have to file an Annual Report and accounts with the Commission unless specifically requested.

All PCCs, registered and excepted, must, however (under the Church Representation Rules) send a copy of the annual report and accounts to the Secretary of the Diocesan Board of Finance, within 28 days of the PCC's Annual Parochial Church Meeting. They must also be provided to the public upon written request (a fee may be charged). PCCs are charitable bodies and may, inter alia, claim tax refunds on Gift Aid contributions, receive investment income without deduction of income tax and in general enjoy all the other tax reliefs available to registered charities.

1.14 Basic overview of PCC accounts

In preparing their accounts PCCs must:

• account for their incoming resources and the investment or expenditure of their resources in at least three main categories: unrestricted funds, restricted funds and endowment funds;

• aggregate the accounts of any other parts of the organisation that the PCC controls;

• account for their stewardship of those resources:

- either in cash-based accounts, consisting of Receipts and Payments account(s) with a Statement of Assets and Liabilities, distinguishing any endowed or other funds restricted under trust law;

- or in accruals accounts, which show a true and fair view, consisting of a SOFA, a balance sheet and notes to give certain additional information;

• identify and, if accruals accounts are prepared, put a proper value on their assets, to help the public understand the PCC's financial position;

• report on their finances and activities in such a way that the general public can understand what has been going on;

• have the accounts scrutinised by an independent examiner if they are not required to be audited by a registered auditor, under the Charities Act and the Church Accounting Regulations.

1.15 Good presentation points

Financial statements should be transparent so that nothing consequential is hidden or obscured, but as uncomplicated as possible so that they may be easily understood.

• Avoid too much detail

Detailed analyses of all the individual accounts, even in the smallest parishes, can be confusing. Only make reference to what is material and round all figures to the nearest pound.

• Summarise where possible

Summarising different funds in columnar format gives the reader a better overall picture. It also allows a reduction in the number of comparative figures.

• If preparing summarised financial statements

A non-statutory summary, derived from the full financial statements, may be produced to help parishioners understand the finances. There are no longer any rules about the preparation and publication of such summaries in the Charities SORP 2015, but as best practice this guide recommends that information about both the SOFA and the balance sheet should be included. However, the full Annual Report and financial statements should always be available.

• Put any necessary detail in the notes wherever possible

The reader is less likely to be confused by the details when looking at the overall picture.

1.16 What are trust funds and why are they important?

The parish must track all of the money it is given to show that the donor's wishes have been met. As that money comes into the parish for so many different things and in so many different ways, how can it be tracked? The answer is by using 'funds'; accounting records that record money according to the specific purposes for which it was given.

This way of looking at money is well known to many householders who, for example, receive a weekly wage and in order to 'make ends meet' then allocate it to various needs or 'funds':

• giving to 'good causes'

• food shopping

• mortgage or rent

• utility bills

• clothes

• holidays

• and the little bit left over!

The weekly wage has come into one household but it has been allocated for various purposes.

Now let's look at how 'funds' work in a parish where the 'wages' are the money given to us by people who choose to say what the money they have given is to be spent on. For example, in one week:

The normal Sunday collection is received (£450) to keep the parish running, as part of its mission and ministry. It is unrestricted money for the PCC's general purposes, to be used in whatever way the PCC decides. As in a household, most of the money given to a parish is unrestricted.

The same week a special collection is also taken for youth work (£250). This time it is clear that the people who donated it expect their money to be used for youth work. It is restricted money (under trust law). Not even the PCC or the vicar can give permission for it to be used on anything else.

The parish is grateful to receive a legacy of £50,000 for youth work. The will states that this money must be invested, and only the income (interest or dividends) can be spent. This is endowed money and it has been restricted to the youth work, so it can't be used for anything else.

On Monday morning all of the money, a total of £50,700, goes into the bank, and the parish accounts show:

Bank current account receives: £50,700 from giving, and out of this:

• £450 is allocated to the general fund (unrestricted money for spending)

• £250 is allocated to the youth fund (restricted money for spending)

• £50,000 is allocated to the youth endowment fund (restricted money for investing).

All the money your parish receives can be put in one bank account so long as you have recorded to which fund the money belongs. As you spend money you also need to show which fund has been used. for example: whenever money is used for youth work it should normally come out of the youth fund. When the parish electricity bill needs paying it comes out of the general fund.

Finally, if the PCC decides, for example, to spend more on youth work, it can move money from the general fund into a designated fund, in this case the 'youth designated fund'. That money is still unrestricted, so if the roof blows off, the PCC can undesignate the money, and move it back to the general fund to use for repairing the roof!

For more information on types of trust fund, see Chapter 2.